LET'S STAY CONNECTED!

Please complete the form found below so we can stay in touch.

Fields Market with * are REQUIRED. All other fields are optional.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

.png)

.webp)

.webp)

.webp)

.jpg)

.webp)

.jpg)

.png)

.png)

.jpg)

.png)

Please complete the form found below so we can stay in touch.

Fields Market with * are REQUIRED. All other fields are optional.

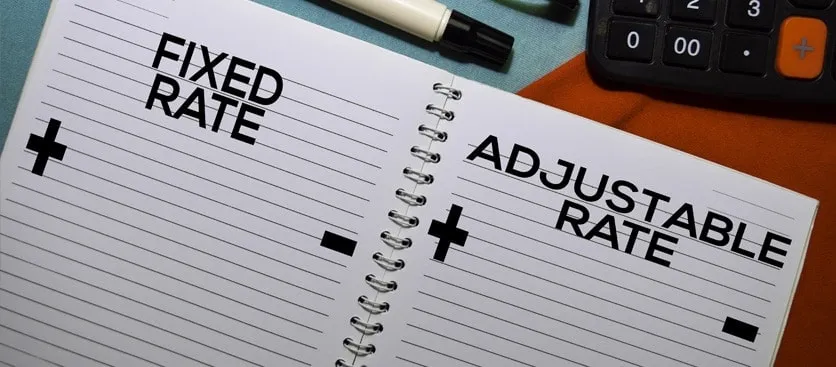

An adjustable-rate mortgage (ARM) is a type of home loan where the interest rate is fixed for an initial fixed rate period, usually several years, and then adjusts periodically for the remainder of the loan term. This means that after the introductory fixed rate period ends, the interest rate can rise or fall based on changes in an underlying index rate, such as the secured overnight financing rate (SOFR) or the prime rate, plus a fixed margin set by the lender.

During the initial period, borrowers benefit from lower monthly payments compared to fixed rate loans because the initial interest rate is typically lower than that of a comparable fixed rate mortgage. However, once the adjustable rate period starts, the monthly mortgage payment can fluctuate with market interest rates. This variable rate mortgage structure allows borrowers to save money if interest rates drop, but it also carries the risk of higher loan payments if interest rates rise.

Adjustable rate mortgages usually have caps to limit how much the interest rate and monthly mortgage payment can increase at each adjustment and over the life of the loan, providing some protection against steep payment increases. The adjustment period refers to how often the ARM interest rate resets after the initial fixed period, commonly every six or twelve months.

Because of the potential for changing loan payments, ARMs are often suitable for borrowers who plan to sell or refinance before the introductory rate period ends, or who expect their income to increase to handle possible higher payments. Understanding how an adjustable rate mortgage works, including the initial fixed rate period, index rates, margins, rate adjustments, and caps, is essential for making informed decisions about choosing this type of mortgage loan.

The difference between fixed interest rate mortgages and adjustable rate mortgages (ARMs) is straightforward. Fixed interest rate mortgages maintain the same interest rate for the entire loan term, providing stable monthly payments that include principal and interest payments. This predictability helps borrowers budget effectively throughout the life of the loan.

On the other hand, adjustable ra

te mortgages start with a lower initial rate, often referred to as a teaser rate, during the initial fixed rate period. After this period ends, the adjustable period begins, during which ARM rates adjust periodically based on an index rate such as the secured overnight financing rate (SOFR) or constant maturity treasury, plus a fixed margin set by the lender. These subsequent adjustments can cause your monthly mortgage payment to fluctuate.

ARMs typically include rate caps, such as initial adjustment caps and payment caps, which limit the maximum amount the interest rate or minimum payment can increase at each adjustment and over the life of the loan. However, borrowers should be cautious of risks like negative amortization, which can occur if the minimum payment does not cover the interest due.

Choosing between a fixed interest rate mortgage and an adjustable rate mortgage depends on your financial situation, including your down payment, loan amount, and how long you plan to keep the loan. ARMs offer the advantage of lower interest rates initially, potentially leading to lower monthly payments, but come with the uncertainty of rate changes. Fixed rate mortgages provide payment stability but may have higher initial rates.

Understanding the differences, payment options, and potential impacts on total interest paid can help you make an informed decision. Consulting with a mortgage professional and seeking tax advice is recommended when considering these loan types.

ARMs are comprised of a few components:

ARMs come with rate caps that insulate you from possible steep year-to-year increases in monthly payments. These caps limit the amount by which rates and payments can change.

Consider a 5/1 ARM with a loan amount of $300,000 and an initial interest rate of 3.5% fixed for the first five years. During this introductory fixed rate period, your monthly payment remains stable and typically lower than a comparable fixed-rate mortgage. After five years, the adjustable period begins, and the interest rate adjusts annually based on the secured overnight financing rate (SOFR) plus a fixed margin set by the lender.

For instance, if the SOFR is 2% and the lender’s margin is 2.5%, the new interest rate would be 4.5%. However, the rate adjustments are subject to caps, such as a 2 percentage point initial adjustment cap and a 1 percentage point subsequent adjustment cap, limiting how much your interest rate and monthly payments can increase each year. Additionally, a lifetime cap restricts the maximum interest rate increase over the life of the loan, providing protection against steep payment hikes.

This structure allows borrowers to benefit from lower initial interest rates and payments, while also limiting the risk of sudden, large increases in mortgage payments during the adjustable period.

To qualify for an adjustable-rate mortgage (ARM) loan, borrowers generally need to meet certain criteria to demonstrate their ability to manage the loan payments. Common requirements include:

Meeting these requirements helps ensure that borrowers are prepared for the potential variability in ARM payments and can manage the risks associated with adjustable interest rates.

Adjustable rate mortgages (ARMs) are typically 30-year mortgage loans, but the duration of the initial fixed interest rate period and the frequency of rate adjustments during the variable rate period can vary significantly. Common ARM loan terms include:

In addition to these standard loan terms, there are three primary types of adjustable rate mortgage loans: hybrid ARMs, interest-only ARMs, and payment-option ARMs. Each type offers different payment options and structures to suit various borrower needs, influencing the monthly mortgage payment and overall loan payments during the entire loan term.

There are several reasons why an adjustable rate mortgage (ARM) may be the right choice for you, such as:

One proposed solution to the potential problem of more borrowing costs as a result of the volatility with SOFR rates is to have households and businesses borrow at a term SOFR rate that is determined in arrears. Although SOFR can be volatile on a daily basis, its one-month moving average tends to be more or less as smooth as 1-month LIBOR. So, a one-month SOFR rate would be the moving average of the daily SOFR rate over the past month. It is not a perfect relationship, and it is important to bear in mind that a one-month moving average of SOFR is inherently backward-looking, whereas 1-month LIBOR is an inherently forward-looking rate. But consumers should not worry the transition is going to have a material impact on their borrowing costs.

This year Fannie and Freddie will begin accepting mortgages backed by the secured overnight financing rate, or SOFR. And after Freddie and Fannie map this out, Orion and others will establish their policies. The FHFA issued a news release that highlighted certain changes affecting single-family and multifamily ARM products. Companies servicing mortgages are also watching these developments. Most existing ARM loans have notes that contain verbiage regarding an index change, and legal staffs are reviewing those as well.